Hey there, bargain hunter.

Start with a fact that doesn’t get enough attention.

The grid-scale battery storage market is on pace to deploy a record 24 gigawatts of new capacity in the U.S. alone this year. Globally, over 353 gigawatt-hours of new storage is expected to come online in 2026. Those numbers are not projections from an optimistic analyst deck. They come from developers who have already broken ground.

That’s the first-order story. More batteries. More storage. More grid stability.

Here’s what Wall Street is mostly skipping past.

Every one of those battery systems requires nickel, cobalt, manganese, and copper. Most of those metals are processed in China. The U.S. imports the overwhelming majority of its refined supply from a geopolitical rival that has been systematically locking up the world’s land-based reserves for two decades.

That is not a supply chain risk. That is a structural dependency with a hard floor and no obvious domestic fix — at least not on land.

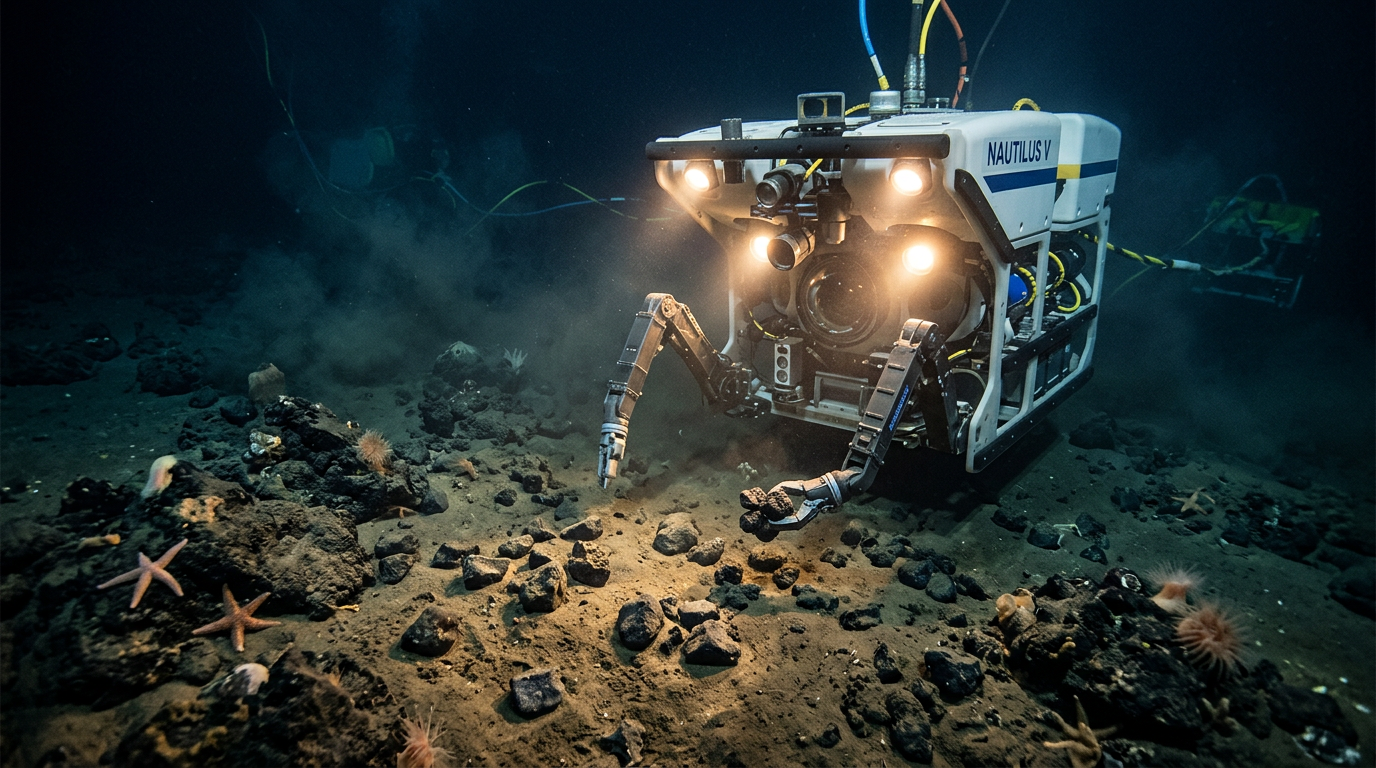

The Thing Hiding Underneath the Pacific

About 4,500 meters below the surface of the Pacific Ocean, in a stretch of international waters between Hawaii and Mexico called the Clarion-Clipperton Zone, there are potato-shaped rocks sitting on the seafloor. Hundreds of billions of tonnes of them.

These polymetallic nodules contain nickel, cobalt, copper, and manganese in concentrations that make most land-based deposits look modest. The oceans contain reserves of these minerals that are many times larger than what remains on land. Scientists have known this for decades. The obstacle was never geology. It was regulation, technology, and political will.

All three of those are shifting at once. Right now.

In January 2026, NOAA issued a modernized regulatory framework for deep-seabed mining under the Deep Seabed Hard Mineral Resources Act. A presidential proclamation formally declared U.S. reliance on imported processed critical minerals a national security risk. The administration directed the Department of Commerce to expedite permitting and the Departments of Defense and Energy to explore offtake agreements to secure seabed minerals.

Nine American companies are now advancing offshore mineral applications. The race for the seabed is not a future story. It is a 2026 story.

Now Here’s Where It Gets Interesting

One company has been building toward this moment for more than a decade. That company is The Metals Company, trading on Nasdaq as TMC.

This is not a startup with a pitch deck and a rendering of a subsea robot. TMC completed a successful pilot collection test in 2022, pulling over 3,000 tonnes of nodules from depths exceeding four kilometers using a vessel called the Hidden Gem. They have conducted 27 offshore resource and environmental research cruises. They have more comprehensive environmental baseline data on the Clarion-Clipperton Zone than any other private entity on earth.

In January 2026, TMC filed the first-ever consolidated exploration and commercial recovery permit application under NOAA’s new framework. That application covers approximately 65,000 square kilometers of the CCZ, with an estimated resource of 619 million tonnes of wet nodules and a potential exploration upside of an additional 200 million tonnes.

The resource estimate includes roughly 15.5 million tonnes of nickel, 12.8 million tonnes of copper, 2.0 million tonnes of cobalt, and 345 million tonnes of manganese.

By March 2026, NOAA determined the application was in substantial compliance. By May 2026, NOAA upgraded that determination to full compliance and moved the application into the certification stage. TMC’s management has expressed confidence the commercial recovery permit could be obtained before the end of Q1 2027.

Slight tangent, but it matters: the permitting process here is not an abstract bureaucratic timeline. It has a clear structure. Substantial compliance, full compliance, certification, Environmental Impact Statement, final determination. Each step is public. Each step has a known sequence. That transparency is itself unusual in a sector where timelines tend to evaporate.

Why Nobody Is Really Talking About This

CNBC is not leading with TMC because there is no earnings beat to react to. The stock does not have a quarterly revenue cycle that triggers analyst upgrades. It has milestones. Regulatory milestones that move on a government schedule, not a Wall Street one.

That mismatch between milestone-driven value creation and earnings-driven media coverage is exactly where the mispricing lives.

TMC also signed a commercial production agreement with Allseas in May 2026, a global leader in offshore pipeline installation and heavy lift. Allseas will develop and operate the first commercial nodule collection system. That contract matters because it transforms the project from a theory into a contracted engineering program with a commercial partner that has already proven it can execute the offshore collection piece.

The company’s preliminary feasibility study for its initial production area carried a net present value of $5.5 billion. As of Q1 2026, TMC had approximately $164 million in liquidity available from cash and credit facilities.

The Risk Is Real. So Is the Asymmetry.

Let’s not gloss over what can go wrong. TMC does not yet have its commercial recovery permit. The Environmental Impact Statement process is underway, and the final determination is expected before Q1 2027. There is no guarantee the permit is granted on that timeline. Environmental opposition is real. The deep ocean ecosystem is not well understood, and that uncertainty is a legitimate risk — not just for regulators but for public acceptance of the project.

The company is pre-revenue. It has been burning through capital for years. Operating costs and research expenses continue. Investors need to understand this is a pre-commercial asset with significant execution risk between here and first production.

But here is the question worth sitting with.

If the permit comes through before Q1 2027, and TMC begins commercial recovery operations targeting a resource base with an NPV calculation in the billions, at what point does the current valuation reflect that?

The battery storage wave is already here. Fluence Energy, one of the largest grid-scale storage integrators, reported a record $5.6 billion contracted backlog as of March 2026, with order intake doubling year over year. Developers are adding a record 24 GW of utility-scale battery storage in the U.S. this year alone. Every gigawatt-hour of that storage needs feedstock. Most of that feedstock still runs through Chinese processing infrastructure.

The structural demand for what is sitting on the floor of the Pacific is not speculative. The uncertainty is whether TMC gets to be the one to bring it up.

That’s a different kind of risk than a money-losing tech company hoping the market eventually shows up.

The market is already there. The permit is what’s left.